Does this differential go back to what happened in the 1970s and 1980s when the Federal Reserve struggled with explosive inflation?

by Wolf Richter about Wolf Street.

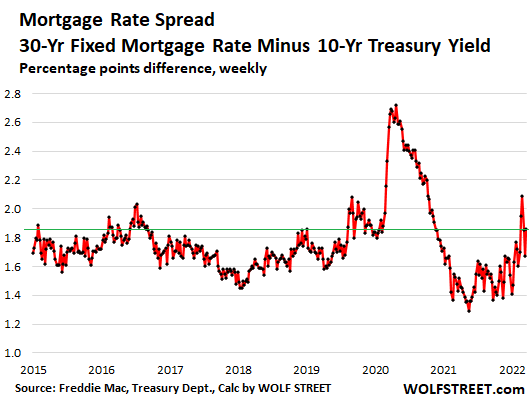

The average 30-year fixed-rate mortgage tracks the yield of a 10-year Treasury, running roughly in parallel but higher. It tracks a 10-year yield because the average 30-year mortgage is paid off in just under 10 years, either through home sale or through reference. But they’re not moving at a steady pace, and the difference between the two — the spread — is widening sharply, with mortgage rates suddenly rising much faster than the 10-year yield.

The 10-year US Treasury yield has soared since the Fed took its infamous “pivot” in the fall of 2021, from willful and tireless disregard for incredibly massive inflation to actually acknowledging, even if initially tepid, its existence and persistence. .

Back in August 2021, the 10-year bond yield was still around 1.3%. Today it is 2.34%, having gained 1.03 percentage points in seven months. Over the same period, the average 30-year fixed-rate mortgage rate, according to Freddie Mac tracking, jumped 1.55 percentage points, from 2.87% to 4.42%:

The chart above shows what happened during the chaos of March 2020, when the Fed cut its policy rates to nearly 0% and announced a massive quantitative easing program that caused the 10-year Treasury yield to fall (green line), while foreclosure rates continued real estate. Systematic deterioration that lasted until December 2020.

This drop in mortgage rates began in late November 2018, when Powell, who was being battered daily by Trump, capitulated and reported that the Fed would soon stop tightening.

At that time, inflation was less The Fed’s goal, the Fed was raising rates that were already above CPI has been cutting its balance sheet at a rate of about $50 billion per month (QT). Housing was damaged, stocks were plummeting, and Trump, who had acquired the Dow, owned it.

The fact that the 10-year yield in March 2020 while mortgage rates were slowly declining only caused the difference between the two to blur. It reached a maximum at the end of April at 2.73 percentage points.

The 30-year average fixed-rate mortgage rate continued to decline until it reached a historic low in December 2020 at 2.66%.

But the 10-year Treasury yield started rising four months before mortgage rates started rising, rebounding from a historic low of 0.55% in August, narrowing the spread between the two. By December 2020, when mortgage rates were at their lowest, the 10-year Treasury yield rose to 0.9%. The difference continued to narrow until 2021.

Part of what contributed to lower mortgage rates in 2021 was the narrow difference between the 10-year Treasury yield and 30-year mortgage rates. At that time, its range was between 1.3 percentage points and 1.6 percentage points.

But in January 2022, the spread suddenly began to widen, as mortgage rates rose much faster than Treasury yields. As of the latest weekly mortgage rate, the spread is 1.81 percentage points, after reaching 2.09 percentage points in early March. Note the increased volatility in the spread:

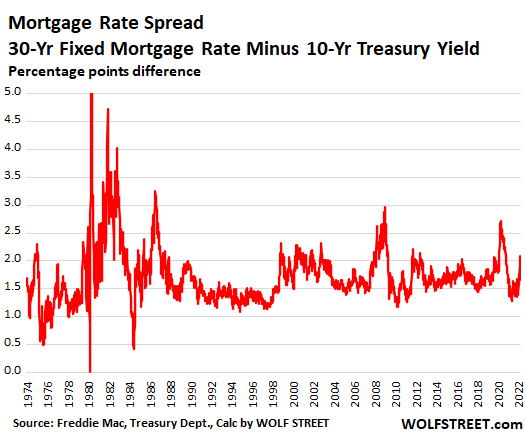

Long-term patterns show how wide the spread is. The massive expansion occurred in March 2020 and during the financial crisis due to the strength of the Federal Reserve pushed down Treasury yields are delayed while mortgage rates.

But in the period between the mid-1970s and the mid-1980s, the Federal Reserve was very powerful Pay Treasury yields to fight the markets are huge Rising prices. Mortgage rates in 1980 – like today – were way ahead of the 10-year Treasury yield as lenders were trying to deal with inflation. Ultimately, Treasuries faltered, then there were massive price cuts, followed by more massive price increases, followed by massive price cuts, and the spread exploded and shrank with massive swings:

The current situation – the unbelievably hyperinflation that the Fed is getting serious about – is much closer to the scenario of the 1970s and 1980s, than it is to the financial crisis and the March crisis of 2020. Over the last two years, the spreads have widened as the Fed has pushed Treasury yields down. While mortgage rates are late. Now the difference is widening because mortgage rates are going up faster than the 10-year yield. The spread is likely to be very volatile, and potentially very wide for certain periods, with mortgage rates likely to exceed Treasury yields by a wide margin during these periods, before Treasury yields catch up or mortgage rates decline.

Enjoy reading WOLF STREET and want to support it? Use ad blockers – I totally understand why – but would you like to support the site? You can donate. I appreciate it very much. Click on a mug of beer and iced tea to learn how to do it:

Would you like to be notified by email when WOLF STREET publishes a new article? Register here.

![]()

More Stories

JPMorgan expects the Fed to cut its benchmark interest rate by 100 basis points this year

Shares of AI chip giant Nvidia fall despite record $30 billion in sales

Nasdaq falls as investors await Nvidia earnings